Saving Your First ₹100,000: The Ultimate Roadmap to Your First Financial Milestone (2026 Guide)

“The first ₹100,000 is the hardest. The second comes much faster because you’ve already built the habits.”

Saving your first ₹100,000 (₹1 Lakh) is one of the most rewarding financial milestones in life. It isn’t just about accumulating money—it’s about developing discipline, building confidence, and creating a strong financial foundation.

Whether you’re a student, a fresher, a salaried employee, a freelancer, or someone just starting your financial journey, this guide will show you exactly how to save your first ₹100,000 without sacrificing your lifestyle.

By the end of this article, you’ll have a practical roadmap, actionable strategies, and a realistic timeline to achieve your first lakh.

Why Is ₹100,000 Such an Important Milestone?

Many people underestimate the significance of saving their first lakh.

In reality, it represents something much bigger than the amount itself.

Saving ₹100,000 means:

- You’ve developed healthy financial habits.

- You understand budgeting.

- You know how to delay gratification.

- You’re financially more secure.

- You’re ready to start investing seriously.

- Unexpected expenses become less stressful.

Think of it as crossing the first mountain in your financial journey.

Once you’ve reached it, the next milestones become much easier.

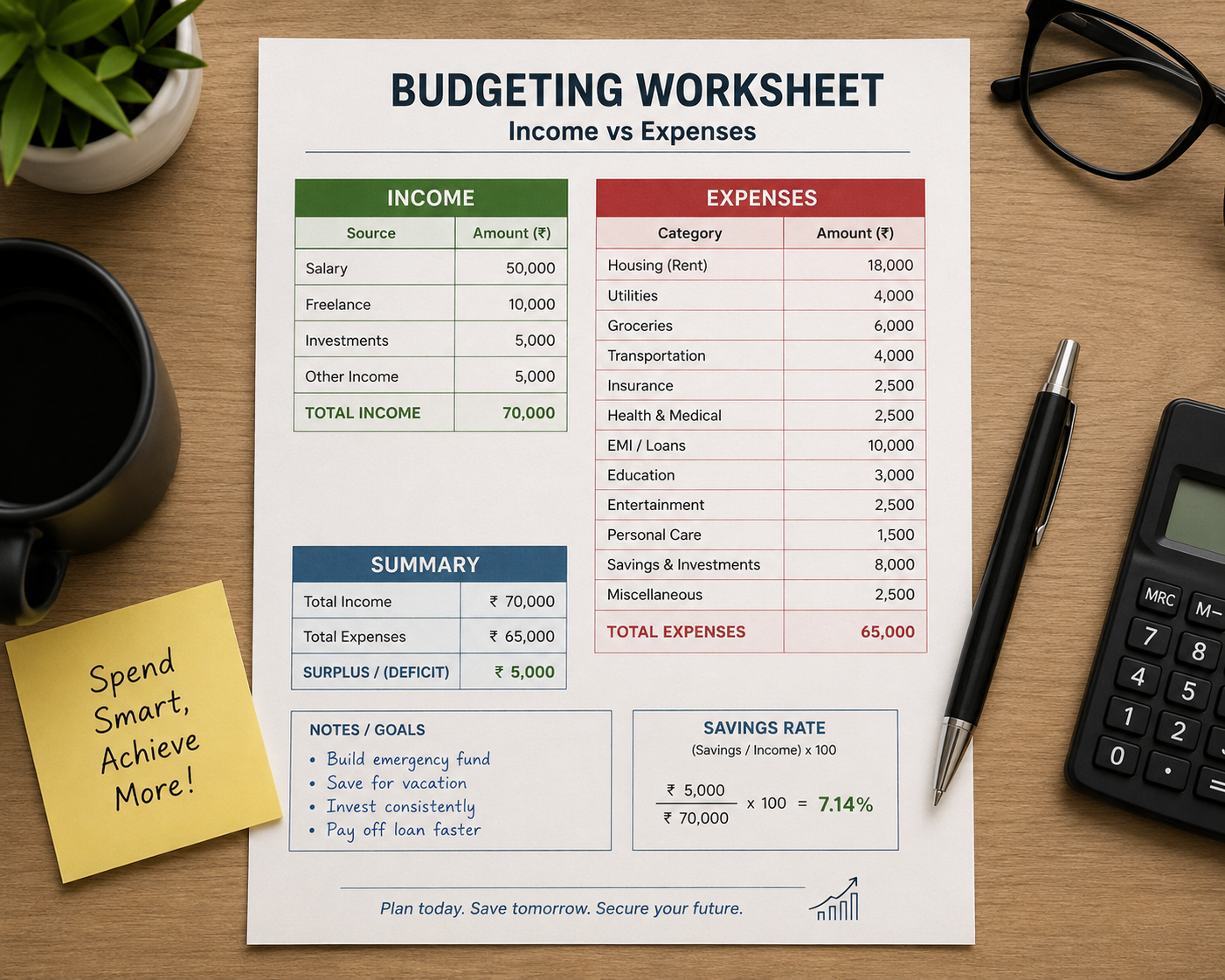

Step 1: Know Your Current Financial Position

Before you save money, you need to understand where your money goes.

Ask yourself:

- How much do I earn monthly?

- How much do I spend?

- What are my unnecessary expenses?

- Do I have debt?

- How much do I currently save?

Create three categories:

Income:

- Salary

- Freelance income

- Bonuses

- Side hustles

- Rental income

Fixed Expenses:

- Rent

- EMI

- Internet

- Insurance

- Transportation

Variable Expenses:

- Dining out

- Shopping

- Entertainment

- Online subscriptions

- Travel

The difference between your income and expenses is your saving potential.

Step 2: Set a Clear Savings Goal

Instead of saying, “I’ll save money.” Say, “I’ll save ₹100,000 within 12 months.”

Goals work because they create urgency.

Example:

Target Savings: ₹100,000

Time: 12 months

Monthly Savings Needed:

₹100,000 ÷ 12 = ₹8,334

If your timeline is:

- 24 months → ₹4,167/month

- 18 months → ₹5,556/month

- 10 months → ₹10,000/month

Breaking large goals into monthly targets makes them manageable.

Step 3: Follow the 50-30-20 Rule

One of the easiest budgeting methods is the 50-30-20 Rule.

50% Needs

- Rent

- Food

- Bills

- Transportation

30% Wants

- Movies

- Restaurants

- Shopping

- Vacations

20% Savings

- Emergency fund

- Investments

- Financial goals

If possible, increase savings to 30% or even 40% until you reach ₹100,000.

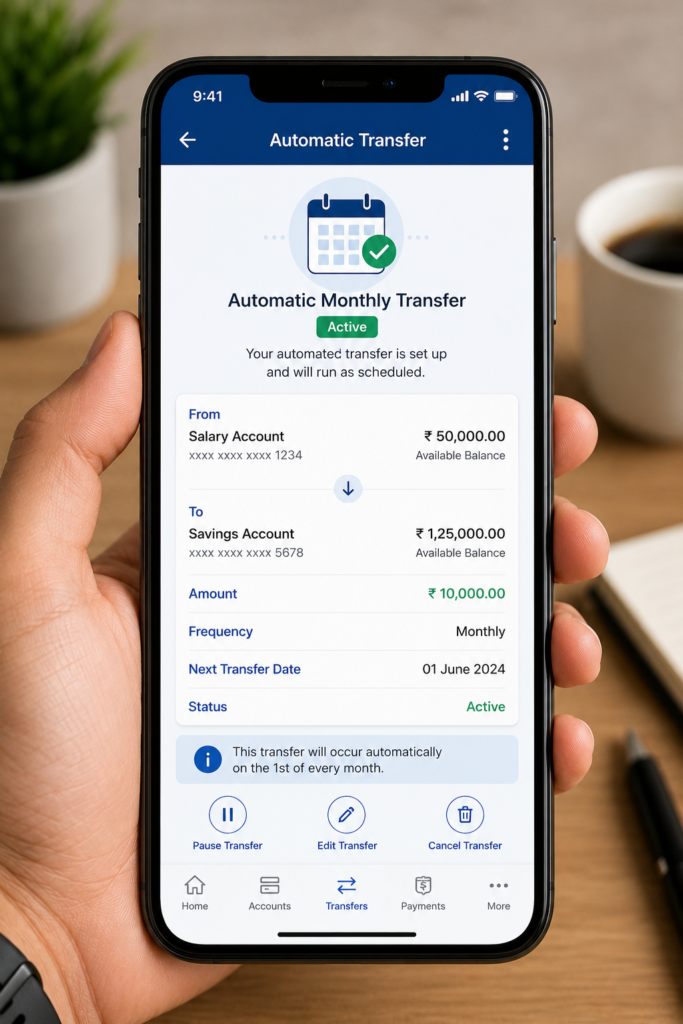

Step 4: Pay Yourself First

Most people save what’s left after spending.

Successful savers do the opposite.

The formula is:

Income → Savings → Expenses

As soon as your salary arrives:

- Transfer savings automatically.

- Don’t wait until the end of the month.

Automation removes temptation.

Step 5: Build an Emergency Fund First

Before investing aggressively, create a basic emergency fund.

Start with:

- ₹20,000

- Then ₹50,000

- Eventually 3–6 months of expenses

Why?

Life is unpredictable.

Medical emergencies.

Job loss.

Car repairs.

Family emergencies.

Without emergency savings, you’ll rely on credit cards or loans.

Step 6: Cut Expenses Without Feeling Miserable

Saving money doesn’t mean living poorly.

Instead, remove unnecessary spending.

Examples:

Cancel Unused Subscriptions

Many people pay for:

- Netflix

- Prime Video

- Spotify

- Gym memberships

that they rarely use.

Review subscriptions every three months.

Cook More Meals

Ordering food: ₹350/day

Cooking: ₹120/day

Monthly savings: Around ₹6,000.

Limit Online Shopping

Before buying something:

Wait 48 hours.

Most impulse purchases disappear after two days.

Avoid Lifestyle Inflation

When income increases:

Don’t immediately upgrade:

- Phone

- Car

- Apartment

- Clothing

Increase savings instead.

Step 7: Increase Your Income

There’s a limit to cutting expenses.

There’s almost no limit to increasing income.

Ideas include:

- Freelancing

- Content writing

- Graphic design

- Teaching online

- Affiliate marketing

- Selling digital products

- Blogging

- Photography

- YouTube

- Stock photography

Even an extra ₹5,000/month reduces your saving timeline significantly.

Step 8: Avoid High-Interest Debt

Credit card debt can destroy your savings journey.

Example:

Credit Card Interest:

36% annually.

Savings Account Interest:

2–4%.

You lose money by saving while carrying expensive debt.

Prioritize paying off:

- Credit cards

- Personal loans

- Payday loans

Step 9: Keep Savings Separate

Don’t keep savings in the same account you use daily.

Instead:

- Separate savings account

- Liquid mutual fund

- High-interest savings account

When money isn’t easily accessible, you’re less likely to spend it.

Step 10: Start Investing Once You Build Savings

Saving protects money.

Investing grows money.

After building an emergency fund, consider:

- Mutual Funds (SIP)

- Index Funds

- Fixed Deposits

- Public Provident Fund (PPF)

- National Pension System (NPS)

The earlier you invest, the more time your money has to grow through compounding.

Sample 12-Month Savings Roadmap

| Month | Savings Goal | Total Savings |

|---|---|---|

| Month 1 | ₹8,500 | ₹8,500 |

| Month 2 | ₹8,500 | ₹17,000 |

| Month 3 | ₹8,500 | ₹25,500 |

| Month 4 | ₹8,500 | ₹34,000 |

| Month 5 | ₹8,500 | ₹42,500 |

| Month 6 | ₹8,500 | ₹51,000 |

| Month 7 | ₹8,500 | ₹59,500 |

| Month 8 | ₹8,500 | ₹68,000 |

| Month 9 | ₹8,500 | ₹76,500 |

| Month 10 | ₹8,500 | ₹85,000 |

| Month 11 | ₹8,500 | ₹93,500 |

| Month 12 | ₹8,500 | ₹102,000 |

Congratulations!

You’ve crossed your first lakh

Common Mistakes That Delay Saving ₹100,000

1. Waiting for a Higher Salary

You don’t need a huge salary.

You need consistent saving.

2. Ignoring Small Expenses

Daily coffee.

Food delivery.

Cab rides.

Online subscriptions.

Small leaks sink big ships.

3. Not Tracking Spending

What gets measured gets improved.

Track every rupee.

4. Emotional Spending

Shopping when stressed is expensive therapy.

Find healthier alternatives:

Exercise

Reading

Walking

Meditation

5. No Financial Goals

Money without direction disappears quickly.

Key Takeaways

✔ Track every rupee.

✔ Create a monthly budget.

✔ Save before spending.

✔ Automate savings.

✔ Reduce unnecessary expenses.

✔ Increase your income whenever possible.

✔ Build an emergency fund.

✔ Start investing after reaching your savings foundation.

✔ Stay consistent.

✔ Celebrate milestones.